Futures market: LME copper opened at $9,707.5/mt overnight, with the highest price reaching $9,747.5/mt and the lowest price dropping to $9,679.5/mt, finally closing at $9,690.0/mt. It fell by $93.5/mt, or 0.96%, compared to the previous close of $9,783.5/mt. The trading volume was 18,271, and the open interest was 308,330. The overall trend showed a downward fluctuation, with prices experiencing volatility after opening and eventually closing lower. SHFE copper 2505 contract opened at 79,860 yuan/mt overnight, with the highest price reaching 79,940 yuan/mt and the lowest price dropping to 79,430 yuan/mt, finally closing at 79,650 yuan/mt. It fell by 670 yuan/mt, or 0.83%, compared to the previous close of 79,950 yuan/mt. The trading volume was 46,572, and the open interest was 197,696. The overall trend showed a downward fluctuation, with prices fluctuating after opening and gradually declining, eventually closing lower.

[SMM Copper Morning Meeting Summary] News: (1) Trump will announce reciprocal tariffs in the White House Rose Garden on April 2, with details likely to be revealed on Wednesday morning Beijing time. US officials stated that the plan will not include any exemptions (including those related to farmers) and will implement industry tariffs at another time.

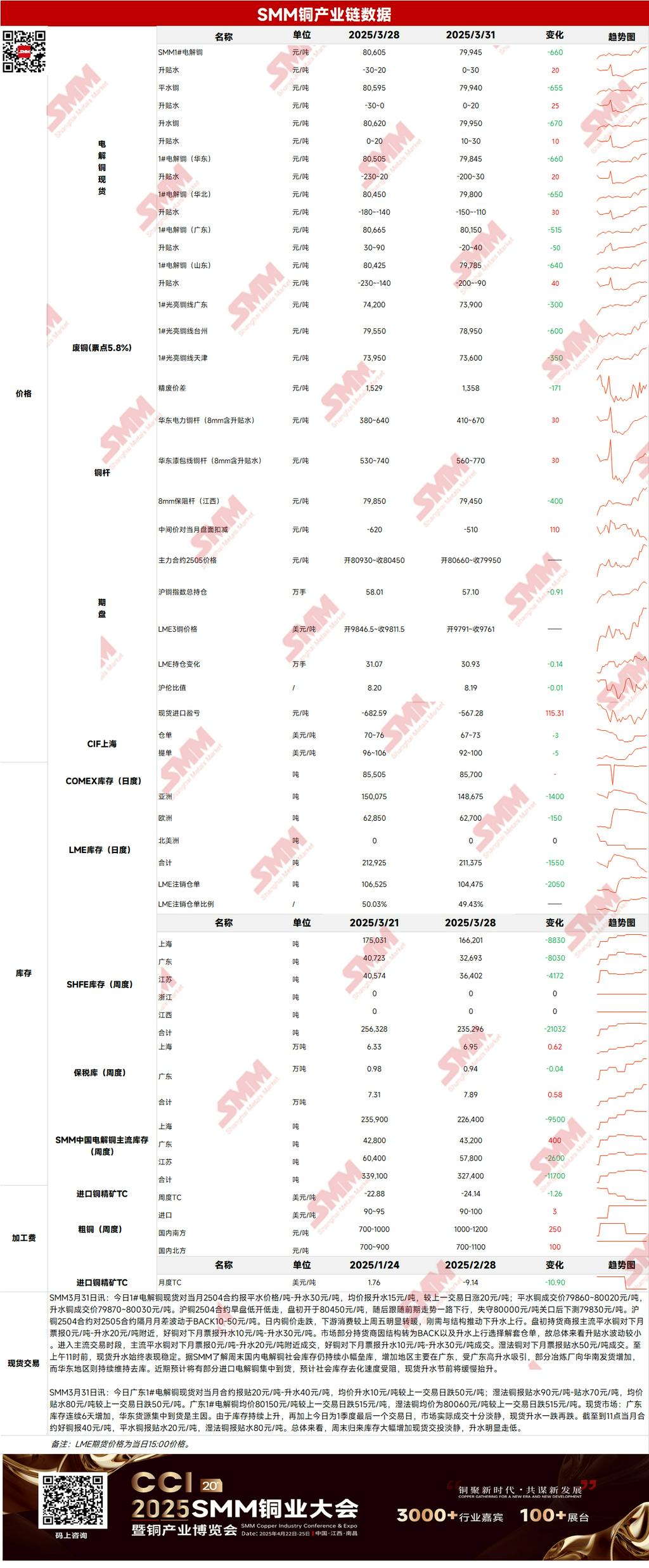

(2) As of Monday, March 31, SMM's national mainstream copper inventories increased by 2,700 mt WoW to 337,200 mt. Compared to the inventory changes from last Friday, only Shanghai saw destocking, while inventories in other regions increased.

Spot: (1) Shanghai: On March 31, spot prices of #1 copper cathode against the front-month 2504 contract were quoted at parity to a premium of 30 yuan/mt, with an average premium of 15 yuan/mt, up 20 yuan/mt from the previous trading day. According to SMM, domestic social inventories of copper cathode continued to build slightly over the weekend, with the increase mainly in Guangdong, attracted by high premiums. Some smelters increased shipments to South China, while East China continued to destock. Some imported copper cathodes are expected to arrive soon, which may slow down the destocking of social inventories, and spot premiums are expected to rise slowly before the holiday.

(2) Guangdong: On March 31, spot prices of #1 copper cathode against the front-month contract were quoted at a discount of 20 yuan/mt to a premium of 40 yuan/mt, with an average premium of 10 yuan/mt, down 50 yuan/mt from the previous trading day. Overall, inventories increased significantly over the weekend, and spot trades were quiet, with premiums declining noticeably.

(3) Imported copper: On March 31, warrant prices were $67-73/mt, QP April, with the average price down $3/mt from the previous trading day; B/L prices were $92-100/mt, QP April, with the average price down $5/mt from the previous trading day. EQ copper (CIF B/L) was $32-42/mt, QP April, with the average price down $3/mt from the previous trading day, referencing cargoes arriving in early to mid-April. Yesterday, the import ratio against the SHFE copper 2504 contract was around -750 yuan/mt, with LME copper 3M-Apr at C$23.69/mt, and the spread between April and May dates at around C$22.81/mt. Market offers and brands were significantly more abundant than last Friday, and suppliers' willingness to sell was higher. It was heard that EQ offers for mid-April arrivals were $35-45/5QP, while domestic warrant offers continued to decline to around $70-75/5QP, with buyers' counteroffers heard as low as $60. It was heard that registered B/L offers for early April were $80/4QP, with prices dropping sharply but buyers' purchase willingness remaining weak. Overall, tariff speculation sentiment has cooled, and the market logic has shifted more towards import profit/loss after the ratio rebounded. In the short term, the arrival of domestic B/Ls has pushed the premium center lower.

(4) Secondary copper: On March 31, secondary copper raw material prices fell by 300 yuan/mt WoW, with bare bright copper prices in Guangdong at 73,800-74,000 yuan/mt, down 300 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,358 yuan/mt, down 171 yuan/mt WoW. The price difference between copper cathode rod and secondary copper rod was 1,050 yuan/mt. According to SMM surveys, as copper prices continued to pull back, some secondary copper raw material suppliers decided to reduce shipments to minimize losses, waiting for copper prices to rebound before selling. Yesterday, the secondary copper raw material market saw average trading.

(5) Inventories: On March 31, LME copper inventories decreased by 1,550 mt to 211,375 mt; on March 31, SHFE warrant inventories increased by 1,729 mt to 137,460 mt.

Prices: Macro-wise, the uncertainty of US tariff policies has created a wait-and-see sentiment in the market, with concerns that US tariffs may harm the global economy. Meanwhile, the CSPT meeting did not reveal more production cut plans, and copper prices fluctuated downward. Domestically, the manufacturing PMI continued to rise, staying in expansion territory for two consecutive months, providing bottom support for copper prices. Fundamentally, under high price spreads, some cargoes flowed from East China to South China, increasing social inventories in Guangdong while destocking in East China slowed. Current consumption recovery is slow, and some imported copper is expected to arrive soon, which may slow down the destocking of social inventories. As of Monday, March 31, SMM's national mainstream copper inventories increased by 2,700 mt WoW to 337,200 mt. Compared to the inventory changes from last Friday, only Shanghai saw destocking, while inventories in other regions increased. Total inventories were 54,000 mt lower than the 391,200 mt YoY. Overall, market sentiment remains cautious, but with improving demand prospects and recovering physical buying, copper prices are expected to find support today.

>Click to view SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct investment research advice. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]